Investment Idea #1: Spire Global (NYSE: SPIR)

Unique capabilities in space supported by excellent long-term economics

This is the first edition of “Investment Ideas,” a segment where I’ll share an actionable stock idea intended for a multi-year horizon. I will track the performance of every idea (updated monthly) here. I will not publish these on any set schedule — only when opportunity knocks (and I’m inclined to write it up). These are not deep dives. My intention is for them to serve as a launch pad for your own research — an idea, not advice.

SPIRE GLOBAL SPIR 0.00%↑

AUTHOR’S UPDATE: Spire underwent a 1-for-8 split on Aug. 31. The split-adjusted price at the time of this idea is $3.60.

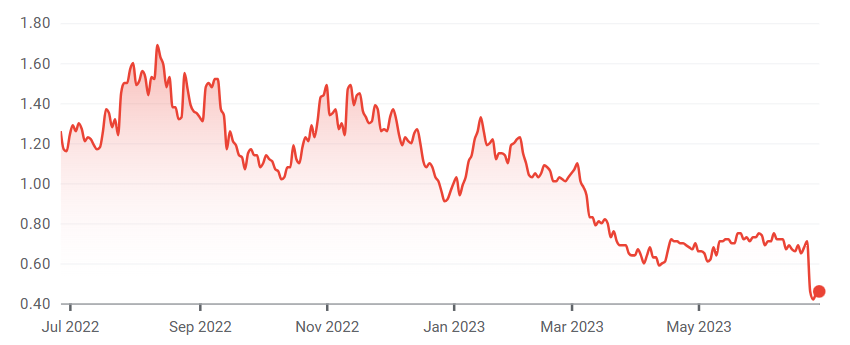

Stock price (as of June 28, 2023): $0.45

Shares outstanding (Class A + B, as of May 1, 2023): 158,121,992

Market cap: $71.2 million

Enterprise value: $117.6 million

Description: Spire sells subscriptions to data feeds from a constellation of ~100 satellites that track maritime, aviation, and weather data. It also offers a Space Services business — modeled after AWS — that offers simple, rapid, and affordable access to payloads in orbit.

Thesis: Spire is too cheap at 1.2x 2023e revenue. It benefits from (1) a 4-5 year first mover advantage, (2) high barriers to entry, (3) an irreplicable data archive, and (4) an end-to-end (customer to space system design) feedback loop. It expects to reach positive free cash flow in Q1-Q3 2024, at which point the market is likely to reassess the value of the business. A 100%+ return by year-end 2024 is reasonable, but expect outsized volatility along the way.

Brief Background

Spire was founded (as Nanosatisfi) in 2012 by Peter Platzer, Joel Spark, and Jeroen Cappaert, three classmates from the International Space University. Platzer’s thesis, in which he discovered two big ideas, formed the impetus for its founding: (1) satellite performance was increasing at an exponential rate (10x every five years), and (2) the incumbent space industry was largely unaware of the trajectory.

Three principles defined the company’s structure from day one:

Collect data only possible to be captured from space.

Collect data only possible to be captured by a constellation of satellites (as opposed to a single one or a small number of them).

Use a software-defined technology architecture (to upgrade satellites in-orbit).

The company built and launched its first satellite through a Kickstarter campaign in 2013. By 2017, the constellation became operational, at which point the company began to scale its subscription business.

In August 2021, Spire went public via SPAC. It raised net proceeds of ~$237 million at an enterprise value of ~$1.5 billion at closing.

In November 2021, Spire acquired exactEarth — its largest competitor in the maritime segment — for $127 million ($102.5 million cash/$24.5 million stock), or ~5.4x revenue. The acquisition significantly reduced the latency of data and brought a 10-year AIS data archive, as well as a lengthy customer list.

Today, Spire’s priority is reaching positive free cash flow by Q1-Q3 2024.

Durable Revenue Growth…

The first hint as to the company’s ability to sustain revenue growth is the rapid pace of historical growth. Spire went from essentially zero to $100 million of ARR in just over 5 years with a relatively lean direct sales motion.

But while the past points to pent-up demand, it’s not a great indicator of future demand. That said, the outlook remains bright because (1) it collects valuable data, (2) it is the only firm to collect such data at global scale, and (3) it benefits from a customer feedback loop that informs product decisions.

It’s easy to get bogged down in the complexity of Spire’s technology. And while it’s a mistake to ignore the complexity (it’s an important layer to its competitive advantage), we don’t need to dive into the specifics behind the technology to arrive at the crux of the matter:

Spire is the only company to monitor every ship and airplane in near real-time (over 200x a day, or roughly every seven minutes)

It collects more of a specific type of weather profile called radio occultation (“RO”) than the rest of the world combined (over 20,000 profiles a day, with potential for 100,000 in 18-24 months)

It offers a simple, affordable way for customers to access sensors on orbit using proven space infrastructure (an AWS-like service for space)

It plays in big markets with a real competitive advantage. Maritime surveillance is a $20 billion industry growing double-digits. Aviation analytics is a $2+ billion market growing in the same range. And weather forecasting is a $2+ billion market also growing around 10% each year.

Spire’s data improves the efficiency of ports and airlines, uncovers illegal fishing/trade, coordinates global supply chains, and enables more accurate weather prediction. Further, the continuous expansion of its archive supports new use cases such as vessel ETA and predictive maintenance models (enabled through the buzzword of today: AI).

On the Space Services side (an $11 billion market expected to reach $40 billion by 2030), several contracts demonstrate the diversity and longer-term potential.

First, NorthStar signed a contract with Spire to monitor space debris. Three satellites are due to be launched in 2023, with pre-agreed options to scale the constellation to dozens of satellites as needed. The contract has potential (not guaranteed) to reach $200 million over time.

Second, GHGSat signed a contract for three satellites that monitor emissions, with expansion clauses that bring the total potential to $100 million over time (again, not guaranteed).

Third, Sierra Nevada Corporation signed an eight-figure contract for four satellites that detect and geolocate objects based on radiofrequency (“RF”) targeting. The global market for such signal intelligence is worth over $13 billion today.

Finally, Ororatech contracted eight thermal satellites (to be launched in 2024) intended for wildfire monitoring. The contract builds on a previous technology demonstration in operation for ~15 months now. Global wildfires created $69 billion of damage from 2018 to 2022.

In all, Spire estimates over 200,000 customers would benefit from use of its data. Today, its roster totals 755 customers. I won’t belabor my point: a large market exists — it’s up to the company to execute given its significant moat. It has guided to 30-36% revenue growth in 2023, which seems a sustainable forward-looking pace given it grew 46% in 2022 with sales headcount roughly flat during the year.

…Drives Improving Economics…

Spire is a data business at the end of the day. Data businesses have some of the best economic characteristics of any type of business. Why? Because the products are sticky and data acquisition costs are fixed, resulting in high incremental margins and substantial profitability at scale. Further, since customers pay for the data upfront, they see their profits in cash.

So why does Spire lose money today?

Put simply, the company is investing aggressively to capture a large long-term market opportunity. Importantly, these investments are focused on technology and product (R&D is 40% of revenue), rather than customer acquisition (28% of revenue). For a new data business, it’s more important to refine products based on existing customer feedback than acquire new customers — so it’s good to know Spire’s focus is on the right area. And we have evidence of execution, with a net retention rate consistently above 100%.

The numbers are a bit noisy given large income statement investments , so I’ll outline a few things I consider more important to the longer-term thesis:

Capital efficiency: Spire’s infrastructure (the constellation) is fully formed and shared by all its business segments. Platzer says the constellation now requires only $10-12 million of ongoing capex each year, which translates into incredible capital efficiency at scale. Incremental capital investments in support of Space Services contracts have attractive ROIs.

Expanding gross margins: Spire’s incremental gross margin over the last four quarters has been north of 90%. Gross margins have jumped from 46% in Q1 2022 to 57% in Q1 2023 as it continues to add customers and upsell existing customers with minimal incremental costs.

Demonstrated operating leverage: Despite bloated public company costs (G&A at 49% of revenue), the company remains confident it can reach free cash flow profitability within a stated timeline of 9-15 months. Operating expenses have steadily declined as a percent of revenue over the last 18 months and remained flat in absolute dollars year-over-year in Q1 2023 while revenue grew over $6 million.

On the Q4 2021 earnings call, Spire put a stake in the ground for free cash flow profitability in 24 to 30 months. It has continued to progress along the timeline since then, and Platzer recently confirmed they remain on track (lightly edited for clarity):

So we're not just talking about EBITDA profitability, operating margin profitability, but actually producing cash flow from our operations… We feel very good about the balance sheet to support that pathway to profitability on the free cash flow basis… And we are excited when we can announce that we have achieved that milestone in the timeframe of 9 to 15 months.

The necessary condition for success is revenue growth and cost discipline, both of which the company has demonstrated an ability to consistently execute on. It’s logical they can continue to do so.

…With Skilled & Aligned (But Imperfect) Leadership

All three co-founders remain at the company, and Platzer retains a 15% ownership stake, with other directors and management accounting for an additional 5% stake. Bonuses are paid out based on the achievement of (1) ARR, (2) non-GAAP operating loss, and (3) revenue per head metrics. This not only incentivizes growth, but responsible growth given the latter two.

I feel management’s skill speaks for itself in building out an unrivaled technological capability, but their managerial and business-building skills may be a blind spot in my analysis given prevailing negative reviews on Glassdoor (3-star rating; 40% approve of CEO; 40% recommend to a friend).

Negative reviews frequently mention “burn out”, an “always-on” culture, high manager turnover, and a “mean and bullying” attitude from senior management. I haven’t spoken to any employees, so I know nothing concrete, but my instinct is this is an issue that merits attention, but does not destroy the thesis.

On the positive side, many reviews — even negative ones — mention “some of the smartest, most passionate people I've ever worked with” / “Extremely strong engineering teams” / “Working with some of the most talented and passionate individual contributors I have ever met” / “Engineers are of an outstanding level,” and further endorsements of the technology side of the business.

Given the hypergrowth of the last five years (128% ARR CAGR), I’m not surprised many employees feel washed out, but it likely doesn’t help when management adopts a hard-driving stance and ignores feedback.

However, this is nothing new; in a 2015 interview, Platzer commented on the culture of “relentless growth”:

Let’s be very clear: we will not change the bar and expectation in terms of performance. We don’t coddle people. People work very hard because they love what they do. And they constantly grow. Not everyone is up for constant growth.

There is clearly an opportunity for cultural improvement, but I do wonder if it’s just growing pains from a break-neck expansion over the last five years. Platzer seems to copy Bezos in more ways than one, which begs an interesting thought experiment: what would Jeff Bezos’ Glassdoor rating have been in Amazon’s early days? (My guess is not too high.)

Conclusion

Spire is a misunderstood, beat-down space stock that’s been lumped in with a bunch of crappy deSPACs. Companies with similar growth, less defensible business models, and worse long-term economics regularly trade at 4-6x revenue (if not higher!). Spire trades at 1.2x 2023 revenue guidance. It’s only a matter of time before the stock reaches a more reasonable level — or the company goes bankrupt. My money is on the former.

Why Does the Opportunity Exist?

First, public markets are skeptical of the viability of commercial space. For decades, space was a slow-moving industry with little commercial appeal. The last decade confirmed this changed, but we still have yet to see confirming evidence of self-sustaining New Space businesses. Public markets (generally speaking) wait to see to believe.

Second, market participants lack an intuitive sense of the addressable market. Who knows how much piracy costs the global economy each year? It’s around $12 billion. Illegal fishing? Around $20 billion. Maritime insurance? $30 billion. What about how many ships are at sea at any point in time? Around 500,000. How many does Maersk (one of the largest shipping companies) own? Just over 700. Spire’s markets are not well known.

Third, Spire is un-investable for most funds. The stock price is <$1, with a market cap of less than $100 million. For funds with no restrictions, they lack liquidity, with shares rarely trading over $1 million of notional volume in a day.

Fourth, Spire went public during the height of the SPAC craze. Over 850 companies went public via SPAC in 2020 and 2021. Many are downright terrible businesses. Spire is not, but it’s lumped in with a tough crowd.

Worthy of Attention

Suspect balance sheet: Spire has long-term debt of ~$120 million (versus cash of ~$73 million) bearing a floating interest rate of ~13% as of Q1 2023. The loan matures in June 2026.

Cash burn: Spire continues to burn cash and reported negative $16 million of free cash flow in Q1 2023. At that pace, cash reserves will be depleted in just over four quarters. That said, cash burn is unlikely to continue at that pace. Platzer has continued to note his comfort with current liquidity tiding the company over until it becomes self-sustaining in 2024. With over a decade of lean operations in the rearview mirror, I take him at his word.

Questionable governance policies: Platzer is married to the COO, Theresa Condor, and they are reimbursed for: (1) two non-business trips to the U.S. each year; (2) housing of up to €5,100 per month; (3) a vehicle for use in Luxembourg; and (4) daycare services when they are both travelling for company purposes. All in, it likely sums to a ballpark $250,000+ in additional compensation — not criminal — but I’m certainly not a fan. That said, I again don’t think it disrupts the fundamental business quality.

Stock-based compensation: Not unusual for a company in the early stages of growth, I think it makes sense for Spire at such an early stage. Compensating employees in cash or stock is essentially a financing decision, and it makes sense for Spire to focus on removing reliance on external capital markets by favoring equity over cash compensation for early employees. Either way, it’s not prohibitively high at 10-15% of revenue over the last five quarters.

Net income margin of -110% on top of a huge pile of high-interest variable debt is pretty scary. With a limited runway, does this thing really have a path to survive? If honestly hard to see.

This aged beautifully.