Investment Idea #5: Thryv Holdings | THRY

A unique, unheralded opportunity in small business America

Author’s Note: In lieu of March’s Recap, I have a new Investment Idea. I think the market today presents some opportunities for investors capable of looking beyond the headlines. The performance of every idea (updated monthly) is here. Keep in mind these are ideas, not advice. Always do your own research.

Thryv Holdings | THRY 0.00%↑

Stock Price (as of April 3, 2025 early trading): $12.10

Market Cap: ~$550M

Enterprise Value: ~$830M

Shares outstanding: 43.3M

Introduction

The fundamental long thesis in Thryv looks similar to what it was a few years ago: a declining, cash cow Yellow Pages business (“Marketing Services”) obscures the growing value of a profitable SaaS business primed to capitalize on a secular change in spend. As SaaS becomes a larger piece of the consolidated enterprise, the stock should reprice.

It sounds good, and management has executed well. But the stock is still roughly flat over the last five years. So, the key question is why now? What makes this investment likely to work over the next five years?

A few ideas worth exploring:

The transition from single product to multi-product opens up a ‘land and expand’ motion with potential to increase the pace and predictability of growth. The recent strategic shift to accelerate the migration of Marketing Services clients reinforces this new motion by maximizing top of funnel throughput.

Management has the operational chops to bring this transformation to a successful end (rebirth), which will clean up the investor story and attract a much wider buyer profile.

Expectations for the business are depressed. Revenue and gross profit multiples (SaaS only) are the lowest ever. Napkin math DCF based on conservative guidance suggests significant upside.

It’s been a painful ride for shareholders to date, but this transformation story is in the final innings, and the investment opportunity has only ripened. Expectations completely ignore the opportunity for long duration SaaS growth. The stock price over the next five years should look nothing like the last five.

Backdrop: The Small Business Cloud Transition

Small businesses today commonly use paper and pen, Excel, or other point solutions to run their business. Buying behaviors, however, are steadily shifting towards software that allows users to manage their business end-to-end digitally. This change creates opportunity, and Thryv is well positioned to capitalize on an enormous pool of changing spend.

Management estimates ~10M customers fit the SAM globally and ~4M customers in the US. The specific number is not important; the opportunity is massive any which way, and Thryv is just getting started.

It has a well-established local sales presence in the US, Australia, and New Zealand, some presence in Canada, and it recently acquired a reseller network functioning across Europe and parts of Southeast Asia. The global expansion, particularly in Europe, should pick up pace in the next few years.

The impending cloud transition may not occur in linear fashion, but we can be reasonably sure a mass migration is inevitable over enough time. The enterprise segment’s path over the last decade is a perfect analog to understand why: cloud tools are value drivers. They improve the customer experience, reduce manual work, and save time. Small businesses who do not evolve risk losing share to those who do.

Product to Platform: Implications on Growth

For years, Thryv was a one product shop selling a CRM tool (Business Center) to its existing Marketing Services client base. It benefitted from long established relationships, but the tool required some significant process reorganization, and many customers just weren’t ready for that type of involvement. ‘If it ain’t broke, don’t fix it.’

Joe Walsh captured this early phase well on the Q3 2021 earnings call: “Let’s be honest, when we started, this was sales-driven growth. We had a simple product, and we sold the crap out of it.”

The second product, Marketing Center, hit the open market in 2H 2023. Right about the same time, Thryv launched Command Center, a freemium product.

These products fleshed out the platform and laid the foundation for a new product-led growth strategy. With Command Center top of funnel, Marketing Center the foothold, and Business Center the scale-up product, what was previously a high-friction upfront sale now looks like a low- to no-friction initial sale leading directly into an upsell motion.

Since mid-2023, the SaaS business has demonstrated the power of this ‘land and expand’ or product-led growth formula. A few pieces of evidence (all SaaS only):

In Q3 and Q4 2023 alone, Thryv added the same number of net new clients as the prior 18 months combined.

In 2024, Thryv added more net new clients (organically, excluding Keap) than the prior six years combined.

Seasoned net dollar retention rate improved from an average of 90.8% in Q3 2022 to Q2 2023 to an average of 96.8% over the last four quarters.

The number of clients with multiple paid centers has grown from just over 1,000 in Q2 2023 to almost 14,000 at year end 2024.

In 2024, the number of clients with multiple paid centers more than tripled.

Gross margins have expanded from ~63% in Q2 2024 to ~73% in Q4 2024.

EBITDA margins have improved from ~10% in Q2 2024 to ~17% in Q4 2024.

Mid-2023 was an important inflection point in the business. After several years of funneling investment into product and technology, Thryv started to deploy it on the playing field. I think the results speak loudly. The platform is coming together, and the product-led motion is gaining momentum.

With the right platform and the right upsell motion, the logical next step was / is to accelerate the pace of legacy client conversions in order to maximize their lifetime value.

One thing is clear: Marketing Center is the right bridge product to drive those migrations. We can see the fit in the step-change in new client growth, but logically it makes sense because Yellow Pages clients are already buying leads; Marketing Center simply sells them leads through a modern interface. It’s not much of a leap, whereas CRM was quite a bit of a hurdle.

I see (at least) three reasons why it makes sense to push the lever even further.

First, the upsell motion is working; maximizing the top of funnel should effectively translate into more durable revenue growth and better economics. Seasoned ARPU is reliably growing mid-double digits. Net dollar retention is now hovering around the target 100% mark. Multi-center clients have tripled in the last year, and these incremental sales carry gross margins north of 80%.

“We are seeing a steady conveyor belt of growth once our customers get in and bedded down. And we have a defined, kind of automated process that's working. It's not happening by chance. So please don't worry about ARPU. ARPU, we've guided, is going to go from about $4,000 a year to about $7,000 a year. All that's still in place.”

— Joe Walsh, Q4 2024 earnings call

The Keap acquisition also plays right into the expanded role of Marketing Center as a foothold product. Its automations directly complement the lead generation capabilities of the product and, over time, should be integrated directly into the platform for a more seamless, automated upgrade path. It makes sense why management expects $50M in cross-sell opportunity over the next three years (2025-2027).

Second, Command Center is rapidly generating a second client ‘zoo’ from which to hunt for new clients. In just over a year post-launch, Command Center has amassed more than 50,000 free users. Several years from now, the freemium zoo will be capable of replacing the current legacy zoo, so Thryv might as well penetrate the current group as quickly as possible before it depletes.

Third, by converting clients to the new SaaS platform, Thryv can also shut down decades-old legacy marketing tech platforms. The result of dozens of acquisitions over the years, these platforms cost quite a bit to maintain.

We don’t have direct quantification of potential savings, but the rough story is there will be some incremental cost associated with actually decommissioning the systems this year, but in 2026 and beyond, the business will benefit from the permanent removal of a not-insignificant cost item.

Really, the whole story hinges on executing the new growth model. Opening the floodgates unlocks greater upsell opportunities across a larger customer base while removing some cost from the business. But it all comes down to execution.

Threats: Churn and Sales Productivity

As I see it, the two biggest threats are (1) elevated churn and (2) a drop-off in sales productivity after emptying the zoo.

Churn is always a concern in the small business segment, but Thryv has kept churn at “world class” levels over the last few years. The reason to think it might climb higher is because of the “forced” migration of some legacy customers.

At least in year one, the churn profile for new conversions was in line with the broader business. But if the economics were to start to deteriorate, I’m confident in Joe Walsh’s ability and willingness to pivot the strategy. They’ve done it before, and I have full confidence they’ll do it again.

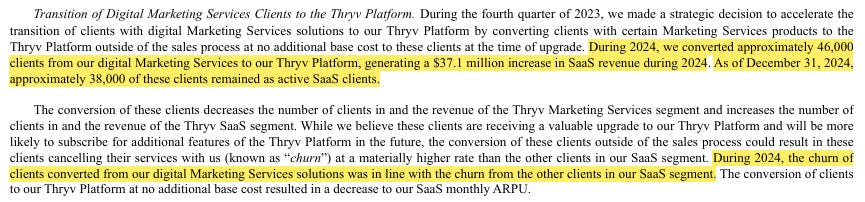

From the 2024 10-K:

Essentially, Thryv converted 46,000 subscribers from Marketing Services to SaaS in 2024, 38,000 of which remained active at year end. But, the whole SaaS business only added 33,000 net new subscribers organically in the year. So, ex-migrations, the business lost 5,000 subscribers.

That implies referrals, the freemium funnel, the reseller network, inside sales, and other outbound efforts yielded net negative customer additions. My question is: what will happen to sales productivity when the zoo runs empty?

I think this is a case of incentives dictating action. In Q1 2024, management re-oriented the sales team’s compensation to pursue multi-center deals; Joe Walsh said at the time, “we moved the needle quite a bit.”

In effect, the conversions are completed outside of a traditional sales process, and the sales team is charged with expanding those accounts once converted. I’ve said it a couple times now, but multi-center clients more than tripled in 2024, growing from 6% to 12% of the base, alongside a >50% increase in the overall client base.

I think the sales team is still highly productive today; Thryv is actually known for a culture of sales excellence. This year, the team was simply targeting a different mission. Move the incentives back over towards signing new customers, and I think we see a different outcome.

Plus, by the time the zoo runs dry, the freemium funnel should be ramped up and the kinks worked out, providing another stream of high-intent customers in which to hunt.

Management: Capable & Aligned

Joe Walsh is a talented operator and capital allocator. Much of his leadership team has worked with him in some capacity for decades. He brings a customer obsession and a genuine passion for doing right by small business that flows into the culture of the organization. He has created a tremendous amount of value in previous pursuits, and he is the largest shareholder of Thryv today.

Over ten years ago, he architected this plan for the business and, since then, has executed beyon expectations. I don’t think many people in the board room at Dex Media ten years ago thought it would actually turn into a half a billion dollar SaaS business while the legacy business continued to throw off cash. But it is.

Walsh often talks of Hubspot as the North Star for Thryv. You don’t often hear a public company CEO refer to another public company as the model for how to think about the business’ progression over time, but I actually think this points to Joe Walsh’s savviness.

The best operators ruthlessly copy what works, then execute better than others in their market. Zuck copied Snapchat, Bezos copied Costco, and so on. Walsh has built Thryv with Hubspot in mind, but focused on a customer segment below it. The strategy is working, the execution has been solid, and the business looks like it will continue to benefit from its emulation of the category leader.

What about macro concerns and the prevailing uncertainty of the current environment? Here is Joe Walsh from the most recent earnings call.

“I would say, overall, and I've said this to you before, I don't really feel like our results ride on small business sentiment or consumer sentiment at all. It's really down to our own execution. But you guys often ask me about what's the macro, what's the climate. And I would say it's meh. It's not bad, but there is just a little bit of extra concern now out there in the environment, and it does not really impact our results.”

Walsh has time and again taken ownership of the responsibility to execute, and then executed. In times of uncertainty or cloudy macro conditions, you want to be in bed with the great operators and capital allocators. And that’s exactly what I think Joe Walsh is. Over the last four years since going public, Thryv has exceeded guidance on both the top and bottom line every single time.

An Expectations Mismatch

Investors do not seem to believe Thryv’s SaaS business is as good as it looks on paper. The stock sits around multi-year lows, creating a mismatch between current expectations (the worst they’ve ever been) and future prospects (the best they’ve ever been).

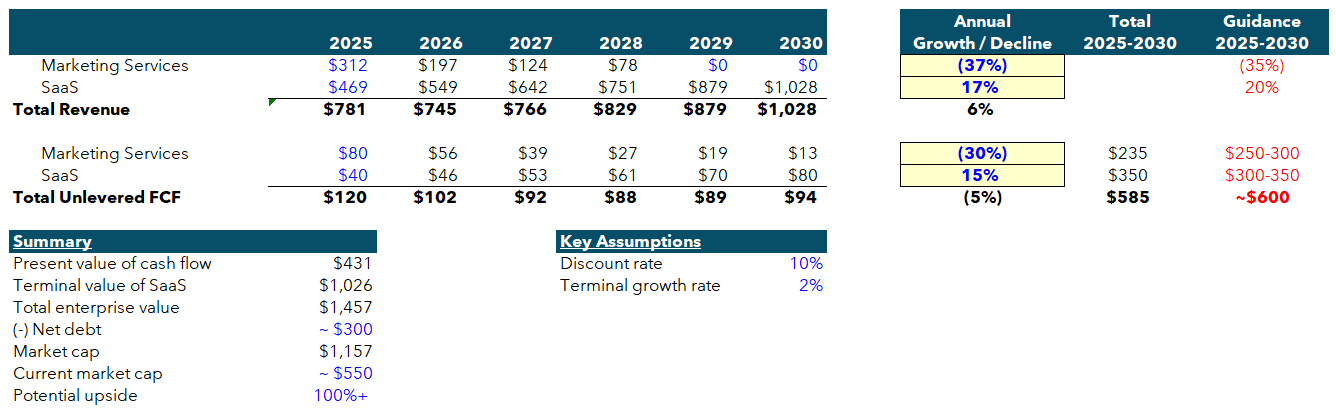

I’m not a DCF guy, but when there is a near-term cash flow play, in addition to a longer duration story, I like to plug some numbers in and see what comes out. As you can see, I prefer napkin math to an in-depth model.

Long story short, Thryv is cheap. The two columns on the right show my estimates of aggregate cash flow from 2025 to 2030 vs. management’s guidance at the 2024 investor day. Mine are right in the middle of the range, but management tends to underpromise and overdeliver.

In 2030, my estimates put the SaaS business’ historical revenue CAGR at ~17% annually (vs. management’s 20% expectation) and free cash flow margin at ~8% (vs. probably 15-20% normalized). From 2025 to 2030, the business should produce cash flow equal to ~80% of its enterprise value.

So, how will the current cheapness become not cheap?

By cleaning up the investor story. By 2027, the business expects to return to consolidated top-line and bottom-line growth. The following year, it will publish the final print directories, which will produce 100% margin cash flow until 2030. And in 2030, Thryv will become a “pure play” SaaS that, inevitably, will re-rate from the current level of expectations.

Most people don’t have the patience to give it five years. I think realistically we won’t have to wait that long, but you have to be willing to do so. The two-year catalyst is consolidated revenue and profit growth. The three-year catalyst is the exit from Marketing Services.

But if Thryv is a good business led by a top-notch management team with lots of room for growth, why wouldn’t you want to own it for the long term?