Welcome to Investment Ideas, a segment where I share actionable stock picks intended for multi-year horizons. The performance of every idea (updated monthly) is here. Keep in mind these are ideas, not advice. Do your own research.

I recommend reading this article alongside my previous analysis of the industry and specific marketplace dynamics.

XOMETRY - XMTR 0.00%↑

Stock price (as of April 5, 2024): $17.86

Market cap: $846 million

Enterprise value: $878 million

At first glance, Randy Altschuler is an unusual candidate to build the next great marketplace. He ran for Congress twice, in 2010 and 2012, and lost both times. But he has a few wins to his name as well.

Altschuler is an entrepreneur. He left Blackstone in 2000 to co-found OfficeTiger, a business process outsourcing company. In 2008, he sold it to RR Donnelley for $250 million. A year later, he co-founded CloudBlue Technologies, essentially a digital waste management business. He sold it to Ingram Micro (public co.) five years later for an undisclosed price.

In 2014, he co-founded Xometry with Laurence Zuriff. Zuriff is a 20-year hedge fund veteran serving on the Center for Strategic and Budgetary Assessments. He’s still Chief Strategy Officer, and the pair collectively own ~15% of the company.

Altschuler and Zuriff are jockeys I’m happy to bet on. They’re proven operators who can execute a business strategy and articulate a clear mission. They’ve made a lot of money in the past, and their motivation goes beyond riches. They take a long-term view to building a service that provides value to a huge industry.

The jockeys are compelling, but the horse is what’s most interesting.

It’s easy to get bogged down in the details of an investment thesis. But simple is best, and the bet on Xometry is simple — so we will keep it simple here.

It’s a marketplace story. The stock is caught up in this year’s guidance and the adjusted EBITDA timeline, and it has suffered as a result. But these things are generally unimportant and this lens ignores what is important — Xometry is a healthy marketplace functioning at scale with early hints of network effects, and it operates in an enormous category uniquely suited to marketplace involvement.

Xometry’s marketplace is thriving. The network is expanding at record pace, buyer acquisition costs are declining, and existing buyers are spending more. A new focus on driving engagement among enterprise buyers is showing early signs of success, and there is plenty of room to further expand wallet share over time.

Recent products such as Teamspace have been met with enthusiasm, all serving to increase marketplace stickiness, which is already impressive — existing customers account for 96% of revenue in any given quarter. And the velocity of product extensions (new processes, materials, and finishes available for instant quoting) is likely to accelerate with the recent Google Vertex partnership. This should enable additional wallet share expansion.

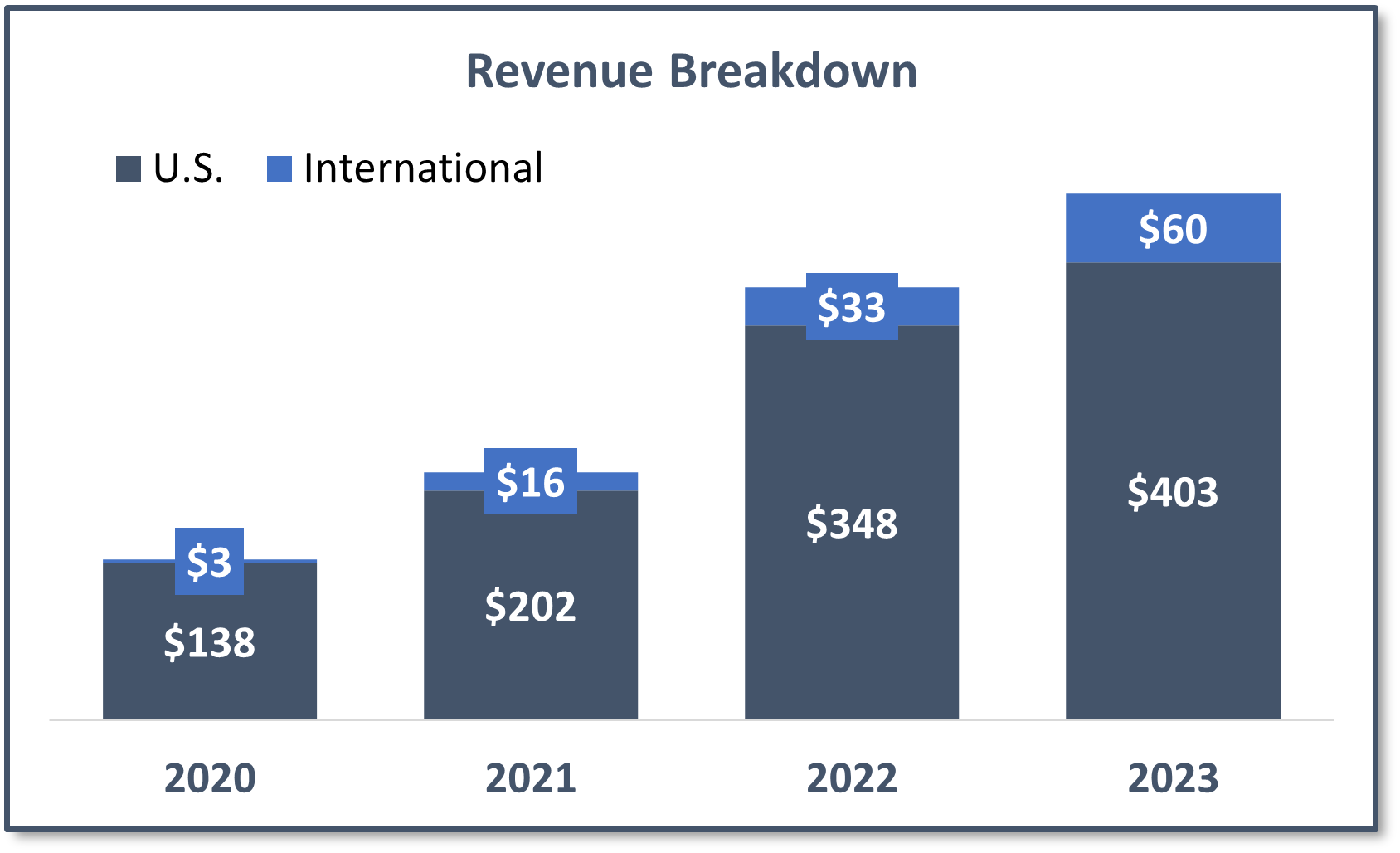

The U.S. business has more than doubled in the last three years. The company launched in Europe in 2019, Asia in 2022, and the UK in 2023. The international business has 20x’d since 2020. It’s now a $60 million contribution, having doubled in each of the last two years.

The future appears bright, but expectations remain low. Custom manufacturing is a $260 billion industry. If in 10 years, Xometry captures just 2% of the market, it will be a $5 billion-plus business. The current valuation, at $850 million or so, ignores the distinct possibility of great success. And, run properly at scale, the marketplace model naturally throws off cash flow.

What protects Xometry from competition? Really, data. The marketplace is built on a proprietary dataset that uses millions of prior transactions to offer an instant price on a custom product. This dataset compounds each day, improving pricing and as a result, gross margins. This in turn drives a greater value proposition to buyer and supplier, gradually moving the market towards efficiency.

Marketplaces are great business models at scale. When they work, they work well. Thus far, Xometry’s results indicate its model is working, and it is rapidly scaling the business. Network effects take time to build, but the leading marketplaces eventually separate from the competition. I have seen little evidence that Xometry can’t build on its competitive advantage in the next decade and further distance itself from competitors who lack comparable scale.

All of this is a direct function of AI — something everyone wants to talk about nowadays — but it bears none of the hype. That’s best-case scenario. AI-enabled applications (in Xometry’s case, think products, materials, and processes) built on top of a unique, proprietary dataset is, in my estimation, a recipe for a durable business. I expect many years of growth in the future.

If Xometry can sustain a 20% top-line CAGR in the next decade, a prospect I consider increasingly likely given the specific dynamics of its marketplace and the compounding utility of its dataset, it will command just over 1% market share. In this scenario, the returns to investors would be excellent, and the prospects for the next 10 years even more attractive.

Ultimately, the proposition is simple. You can buy an AI-enabled manufacturing marketplace built on a unique, difficult-to-replicate dataset. The company is growing quickly, still losing money, but has attractive economics at scale. It is tackling a $260 billion category where it can sustain share gains over a long time and remain a small piece of the pie. And it is run by two sensible and capable operators who think long-term and share ownership of the business.

I’m a buyer.

Thank you for taking the time to read. Please join the discussion and comment with thoughts of your own — especially if you disagree. And if you enjoyed this article, hit like, share, or subscribe to support my continued work.

Tim, did some work on this over the weekend. Still really like the idea/business.. but is there a 6-12 month pitch? Fund won’t care about long term right now. Even re-rate from profitability is a ways away. Thoughts?

I'll let you read it on VIC, but it was written as massively overpriced 2 years ago. So far the SP has went down, as expected, and the thesis revolves around the service not being as needed as suppliers have already developed this capability, and the company being a price taker as the AI essentially could be trained on lower prices and would keep reflecting that for a while