What's Behind the Rise of Crocs?

Understanding the brand's secret sauce

This is meant to be read alongside Investment Idea #2: Crocs. This write-up omits certain aspects that the other includes, and vice versa.

The rapid rise of Crocs seems to mystify many investors. What is its recipe for growth? Can it be repeated? How sustainable are margins? Is it really just a fad? These questions and more are at the forefront of any investigation into Crocs.

The market, for its part, expresses little faith in the brand’s ability to replicate its recent success. From my perspective, this is one of the more pronounced misunderstandings by the market.

The brand’s success is derived from a clear strategy planned and executed by Andrew Rees and Michelle Poole. The duo joined in 2014 and have used a clever combination of (1) product innovation and (2) marketing to orchestrate a highly successful turnaround. These activities are not unique to Crocs — they fuel many successful brands — but the execution at Crocs has been terrific.

In this write-up, I hope to explain exactly what I mean by product innovation and marketing and explore why they are a repeatable value creation formula.

What is product innovation?

The foundation of a good brand is a set of core products that customers love. Consumers are fickle beasts, however, and get bored easily. Consumer products must be updated, tweaked, or otherwise refreshed to maintain their relevance. Apple, for instance, releases a new iPhone every year; Honda makes a new Civic every year; Nike unveils new LeBrons every year; Zara launches a new collection every season, and so on. It happens everywhere in the consumer market.

Crocs is no different. It has four main products — Clogs, Sandals, Jibbitz, and Hey Dude — that are really platforms on which to iterate design and functionality.

The majority of Crocs’ business is Clogs — you know the silhouette.

Clog sales reached $2 billion in 2022, more than doubling since 2020. The clog continues to grow double digits through Q2 of this year.

Sandals are a natural extension of the molded footwear brand. Management has been investing behind sandals for around six years now and has its sights set on north of $1 billion in 2026 revenue (a 36% CAGR from 2023 guidance of $400 million). This year, sandals grew 65% in Q1 and 34% in Q2.

Note “investing” shows up on the income statement in SG&A. The company is extremely capital efficient with capex averaging less than 3% of revenue.

Jibbitz, the personalized add-ons for Crocs, has grown from a $70 million business in 2020 to around $200 million in 2022. Not only is its success evidence of further engagement with the brand (no other footwear company sells a similar product), it’s also a substantial source of high margin revenue.

Hey Dude operates independently from the Crocs brand after being acquired in early 2022. Guidance calls for just over $1 billion of revenue this year (ahead of management’s original target of $1 billion by 2024). The current focus is on building out brand awareness, and management is confident in its global appeal over the long-term. I share a similar level of confidence.

Why? Because Hey Dude’s Wally/Wendy silhouettes share the functional comfort characteristics of the iconic clog, which is responsible for much of Crocs’ success. The brand is a perfect vehicle to continue to execute the product innovation and marketing playbook that has worked so well at Crocs.

This brings us back to our original question: what exactly is product innovation? Really, I mean four activities:

Releasing different colors/patterns/graphics: Crocs sells around 1,000 different SKUs, with most being simple variations of the same core products. A seasonal pipeline of new colors and graphics is table stakes product innovation.

Collaborations: Crocs has partnered with everyone (from Balenciaga to Taco Bell, Luke Combs, Salehe Bembury, and KFC, just to name a few). Collaborations grow the brand among an extremely varied audience and are key to maintaining its relevance globally. (Check out the Crocs collaborations page to see more examples — notice how many are sold out.)

Tweaking product characteristics: This means adding height, a fur lining, or otherwise changing a non-core aspect of the product. The “Croc Madame” partnership with Balenciaga is one example. It’s hideous if you ask me, but it sells (for over $600!). And it builds on the unique distinctiveness of Crocs to expand the number of entry points to the brand.

What do I mean by this? Think about it: the average Balenciaga customer would be unlikely to buy a pair of Crocs if it wasn’t abundantly clear that the pair they own is different — special in some way. Crocs’ adaptability to such demands is important to the overall story.

Targeting specific wearing occasions: The functional characteristics of Crocs make them useful for a variety of professional jobs such as nurses or chefs, as well as activities such as boating. Focusing product lines on these use cases lowers the barrier to entry for potential customers.

At first glance, product innovation is corporate gobbledygook, but it’s quite straightforward. These activities can be executed across the company’s four main products (really three, Jibbitz is more of an add-on business to Clogs and Sandals, but it still abides by all the same principles of product innovation) in order to maintain the brand’s relevance and vitality.

What is marketing?

I think we all intuitively know what marketing is: it’s telling a story about a product that leads the consumer to buy it. Product innovation necessarily feeds the marketing machine because frequent new designs and collaborations are the best source material for new stories under the brand’s umbrella.

Comfort and personalization are the cornerstones of the brand’s story. The marketing team, led by Michelle Poole, is among the best in the business at telling that story. It also doesn’t hurt that Crocs is a polarizing product; as Michelle Poole said, “You love us or hate us. That’s okay, because that means you’re paying attention to us.” It all works to keep the brand relevant and retain consumer mindshare.

So, how does Crocs tell its story? Aside from marketing via its own unique shoe designs, Crocs uses integrated global campaigns and celebrity influencers as the core of a 100% digital marketing strategy. Its slogan is “Come As You Are,” which I think conveys the comfort and personalization message well.

The marketing engine is just picking up steam, too. Total spend reached $260 million last year, more than double 2020 as it continues to scale at a fixed 7-8% of revenue. This marketing spend is the company’s investment in its future — it is how it protects the brand’s competitive positioning. More spend should correlate with a positive outcome over time.

Are they repeatable?

Product innovation and marketing are not complex processes, and they are within management’s control for the most part. Given the people responsible for its turnaround continue to run the company, it’s logical to think they are capable of repeating their successful execution.

Brand collaborations are not entirely in management’s control, but they are unlikely to go anywhere. They’re a good deal for both sides. Partner brands magnify their visibility across the world in a low-risk manner while maintaining an appropriate sense of exclusivity (most collaborations end up selling out). In this area, Crocs’ distribution (in over 85 countries) and widely recognized silhouette create a competitive advantage.

For Crocs, the collaborations extend the brand’s reach across an incredibly varied audience — from the luxury fashionista to the chicken wing lover to the streetwear enthusiast and anybody in between. Both sides win.

Crocs management — who may be one of the most undervalued teams in the market — also believes they can replicate their success. They are confident Crocs can be a $6 billion brand in 2026 (a 26% CAGR from 2023 guidance).

While I think it’s certainly possible, it seems unlikely on that timeline. The current stock price doesn’t demand much, however; shareholders can earn excellent returns even if management misses the target by several years.

How do they create shareholder value?

If the strategy can be repeated, we can expect continued capital efficient growth.

Since 2014, Crocs has reduced its capital intensity while increasing returns on capital and using excess cash flow to opportunistically repurchase shares. The combination has created extraordinary results for shareholders. Since Andrew Rees’ first day at the company in June 2014, the stock has risen from ~$15 to ~$97, a roughly 23% CAGR over nine years.

Note this hasn’t come without a good deal of pain. The stock experienced three 60%+ drawdowns over this period.

Today, Crocs owns and operates 40% fewer stores than it did in 2014 yet sells more than double the pairs of footwear (over 115 million pairs were sold in 2022). It also outsourced all manufacturing, leaving expansions to distribution capacity as really the only capital expense.

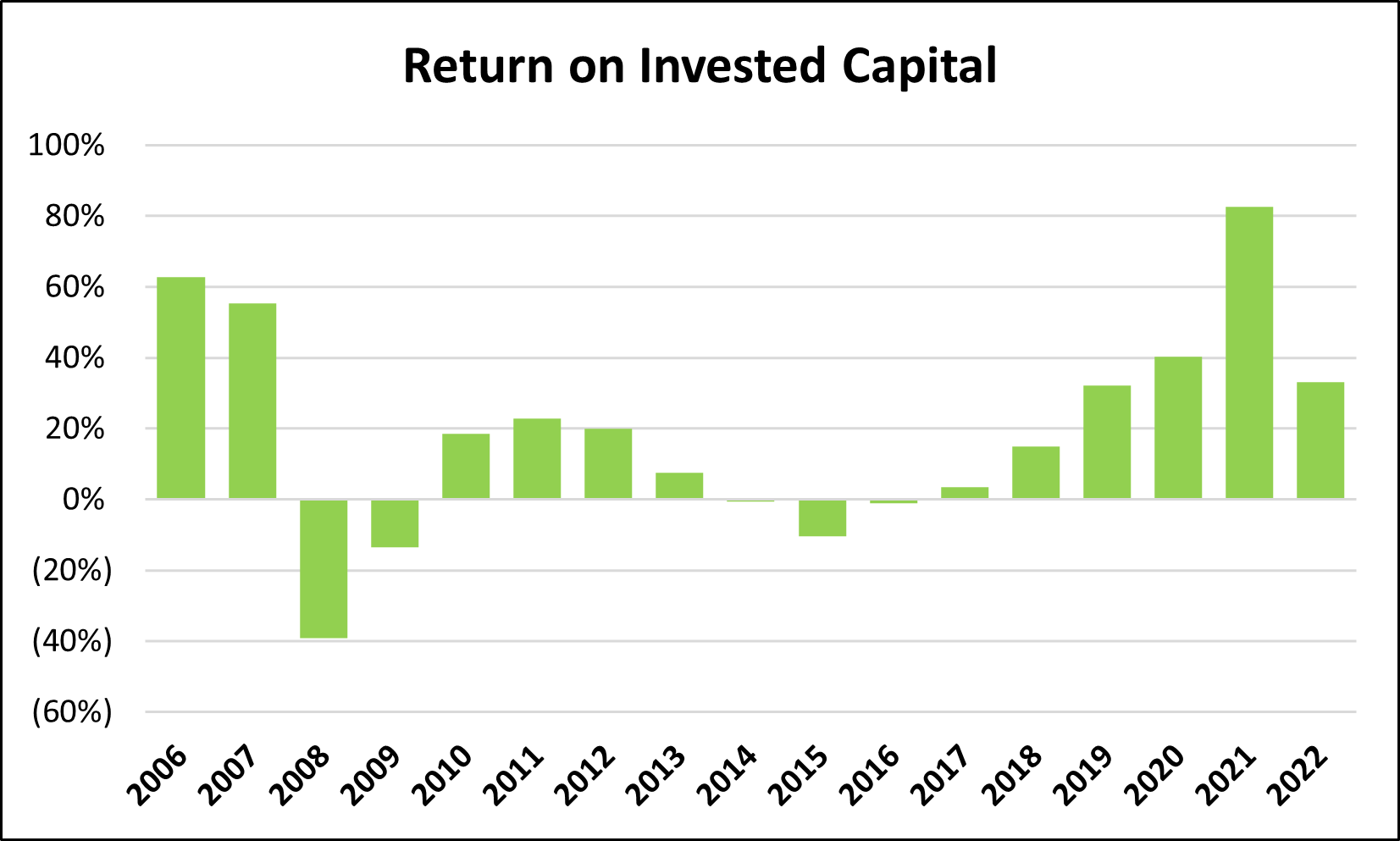

From 2006 to 2013, capex averaged 6.4% of revenue; from 2014 to 2022, it averaged 2.5%.

From 2006 to 2013, net working capital averaged 18% of revenue; from 2014 to 2022, it averaged 8%.

These changes, in addition to the improvement in profitability, have had a profound impact on ROIC. From 2006 to 2013, ROIC steadily declined. In the years since the turnaround, we’ve seen the opposite: a sustained uptrend.

Note that 2022 is impacted negatively by the Hey Dude acquisition, a sizable long-term bet that is in the “investment” phase more than the “returns” phase.

Since Crocs has limited reinvestment requirements and a highly profitable business model, it produces a substantial amount of excess cash flow. Free cash flow totaled nearly $500 million in 2022 and nearly $750 million over the last 12 months.

This cash flow feeds the buyback (and debt repayment) machine, an effective vehicle for returning capital to shareholders. Management has retired roughly 30% of shares outstanding since YE 2013. Moving forward, we can expect more of the same.

Putting it all together

There are a few elements to the story:

Product innovation and marketing fuel the growth of Crocs.

Both are straightforward processes, largely within management’s control.

Given management’s capacity for execution, it is logical they can continue to achieve success.

Returns on capital have significantly improved since 2014, and excess cash flow is used to repurchase shares.

There’s not much to dislike. Sure, Crocs could turn out to be a fad — the future is always uncertain — but it appears to have discovered an effective, repeatable growth strategy. Management is focused on creating returns for shareholders. And Hey Dude is valued as essentially a free option with a high ceiling.

I see a very low probability of losing money over a multi-year time horizon.

Tags: CROX 0.00%↑