Continued thinking on CROX

Maybe the fad risk and acquisition criticisms are overdone

I suspect the lack of trust in Crocs’ fundamentals is downstream of two things: the market thinks the Crocs brand is on the verge of stagnation, and the Hey Dude acquisition is widely regarded as a failure.

The stock continues to be held back, and only some combination of these can provide a rational explanation for why the market persistently undervalues (at least relative to peers) a company that reports such solid numbers.

I’m more positive than most — let me explain why.

The Crocs brand has misunderstood staying power

Readers of my previous articles (investment idea #2 and more analysis) will at least be familiar, but Crocs has a pretty incredible story. Only two years after launch, it broke $100 million in sales; then in 2007, it did almost $850M in sales. For reference, the iPhone launched that same year with sales of $630M (granted, it wasn’t available until June, but the point remains).

Crocs might be one of the most viral consumer product launches in recent history, and the product foundation is extraordinarily simple: a molded clog. This context is at least worth bearing in mind given its recent return to virality.

After somewhat of a lost decade, the brand has had a remarkable run since the pandemic. Crocs will generate around the same revenue from 2021 to 2024 as it did in the preceding ten years. Sales have grown at ~24% per year since 2020 vs. ~3% from 2012 to 2020.

It’s natural to assume the brand’s growth will return to stagnation, just as it did in the prior decade, but I’m not so convinced. Arguments for reversion miss the strategic changes and simplification of the business responsible for its recent success.

My concept of the marketing and product innovation flywheel talks about how continuously refreshing the core product creates an unlimited supply of marketing material to leverage across a wide base of partner brands, influencers, and paid performance channels. This marketing spend is the engine of growth and a strategic priority for Andrew Rees, who joined in 2014.

The strategy, given time, worked, and it has now translated into scale. With scale, higher marketing spend is here to stay. This fact underpins a good chunk of my belief in the brand having some kind of staying power — staying power which I think the market underestimates.

Crocs sells over 100M pairs of shoes in 80+ countries, balanced evenly between wholesale and direct channels. It has established relevance at global scale, created a unique association, and seems highly unlikely to disappear from the storefront or lose consumer mindshare now.

Recent results also refute claims of irrelevance.

Wholesale in North America has been the one weak point, but the declines have been marginal, and management is confident the brand will continue to grow in North America over time. The core clog continues to grow, and sandals is early in penetrating a large category.

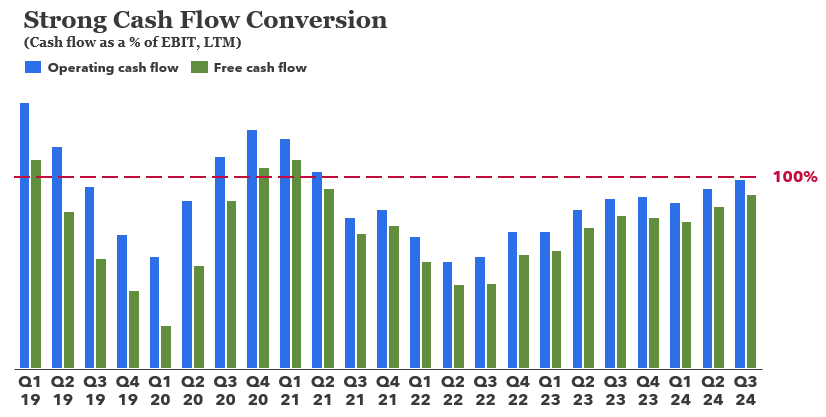

Wholesale’s weakness in North America doesn’t take away from the fact that Crocs is a well-managed brand producing reliable mid-20% operating margins, most of which converts to free cash flow.

I understand the fad risk and the ease with which people can extrapolate marginal revenue declines in one channel in the most mature geo, but I’m not convinced. The foundation is still solid.

China, India, and other large markets are very early in their growth story, and the brand has real momentum abroad. There’s not much to dislike about the core business – there’s actually a lot to like – and management is top-notch.

Hey Dude is just getting started

The Hey Dude acquisition is one of the most commonly cited criticisms of management, and while there is some validity to the argument, I think it overlooks the very real possibility it is simply too early to judge.

No data point proves my line of thinking is correct, but my instinct is based on deep trust and respect for Andrew Rees and the management of the company. I understand their intentions with the brand, its long-term potential, and I believe there is a clear path to executing on that plan over time.

Even the best-laid plan encounters some obstacles, and Hey Dude faces its share today, with several consecutive quarters of declining sales across channels.

Management’s stance on the brand has remained resolute, however, and their conviction in the investment ultimately creating value for shareholders has not changed. I think they have earned the benefit of the doubt.

Crocs ten years ago is a decent proxy for the strategy employed at Hey Dude today: clarify and unify the brand’s messaging, focus on strategic wholesale accounts, clean up the global marketplace presence, sharpen distribution, and develop a unique identity / association.

With Crocs, it worked. I struggle to see why it can’t or won’t work with Hey Dude, which benefits from a larger category to sell into and more wearing occasions to market to.

Financially, the immediate returns have not been good, but it also hasn’t been disastrous. The parent company has already paid down over $800M of debt from the acquisition, and Hey Dude has contributed over $500M of operating income compared to ~$2.2B of operating cash flow at the parent over the same period.

We also know the brand can generate attractive profit margins.

It has not been a home run by any stretch of the imagination, but it’s hardly a strike out. They’ve fouled off a few pitches, but they’re still at the plate. Give the investments in brand marketing and distribution some time to play out, and we could be having a very different conversation in 2-3 years.

There is always a possibility that Crocs’ polarization was the essential ingredient in its success, which would make it difficult to replicate the same playbook at Hey Dude. All publicity is good publicity, and the public’s love / hate relationship with Crocs no doubt strengthened its consumer mindshare over time.

Hey Dude is not such a polarizing brand, but I do think it has distinctive qualities. I’ve even received a few remarks while wearing Hey Dudes out and about, and that’s far from a regular occurrence.

To be sure, it’s anecdotal and probably means nothing, but it’s unusual. The average customer owning four pairs is also unusual, and I like unusual. These facts alone are no reason to invest, but they add a dimension to the conversation.

Several quarters of declining sales are by no means a death sentence to a brand managing a hangover from rapid growth over the last few years. With the return of Terence Reilly to lead Hey Dude, the brand has a sensible management team guiding its trajectory, and I’m excited about what it can do.

Conclusion

I think Crocs has a core franchise which stays stable in North America, grows steadily internationally, and continues to produce reliable cash flows. This cash flow funds international investments and occasional buybacks at sensible prices.

Hey Dude is still an attractively priced option. It’s profitable but has returned to Earth after rapid growth pre- and post-acquisition. The question now is whether management can right the ship and generate an acceptable return on the significant investments in the brand. That’s a bet I’m willing to make.

I continue to see a favorable probability of earning market-beating returns, and I look forward to updating you if anything changes that stance.

Tags: CROX 0.00%↑

Hi Tim. I'm almost entirely in agreement with you and am quite happy I bought a nice fat tranche under $100.

On the subject of HeyDude, I think it's not just the lack of polarisation compared to the Crocs brand that's worrying, but also the fact that the brand hasn't cemented what its core is. If you look at their products for sale, it seems like a free for all in terms of silhouettes; Something needs to change there if the brand is to cement itself imo. I think even if heydude doesn't quite live up to management expectations, the share is cheap. I consider Terrence Reilly at HeyDude to be a free option essentially, and suspect that the growth that will change the narrative will come out of either India, Korea or China. I don't think Japan should be a tier 1 target. Of course, large buybacks also may be a catalyst for share price appreciation.

- Zaheer Jamal