Sonos: More Than Great Sound

What about the brand?

A wise investor would do well to avoid consumer audio. Competition is stiff and often dictated by price (Google and Amazon sell speakers as loss leaders). Suppliers have significant bargaining power (only 3-4 firms make the drivers for most speakers). Product development cycles are long. New entrants are regular. Sales are seasonal. Working capital can swallow cash flows.

It’s a tough business, but it’s not only tough on the operators. Public markets don’t like lumpy results. Investors must handle regular swings in price (and results) with equanimity.

I first bought shares of Sonos in January 2019. Since then, the stock has fallen >25% from highs on four occasions. Twice, the stock has fallen by >60%. Yet at one point, it was up >300%. Today, it sits >65% below highs from April 2021.

When any stock suffers, it prompts reflection. What went differently than I expected? Do I still want to own this business? And a particularly pronounced question in the case of Sonos: why did I invest in a speaker company?

Such questions are good — and necessary — but it can be tempting to turn to the price graph for answers — a cardinal mistake.

So why did I invest in Sonos?

My investment rests on a simple foundation (belief): it has a unique culture of innovation and commitment to quality. Culture and quality lay the foundation for an enduring brand. An enduring brand is the source of pricing power. And pricing power is the source of profits (cash flow).

I may be wrong, of course, but profits don’t arrive overnight, so (as always) we have to live with the uncertainty as it plays out. There is one thing for certain, however: the best brands are built over a long period of repeatedly delivering on a promise to customers.

Here’s why I think Sonos is building an enduring brand:

1. Customers are repeat purchasers

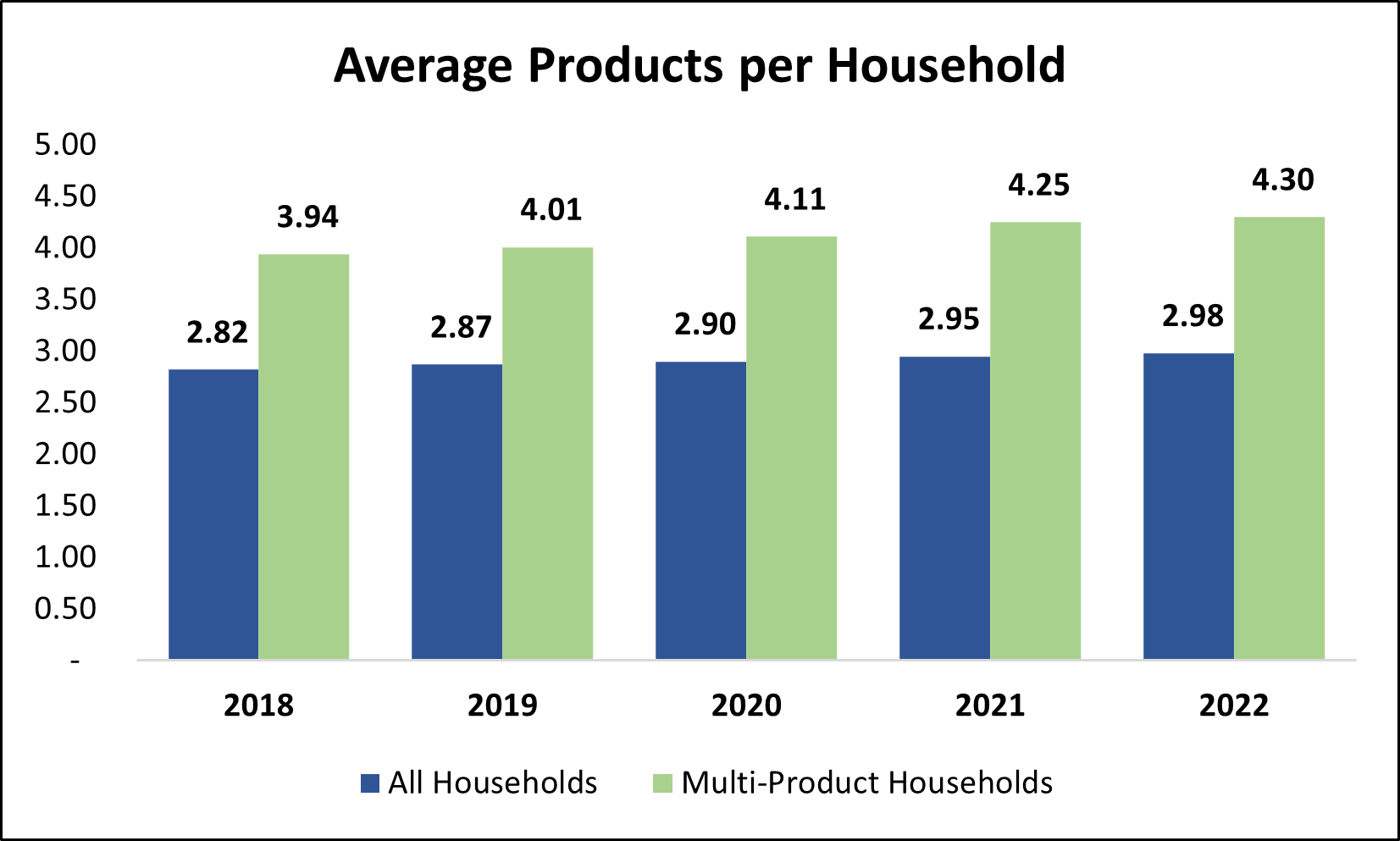

60% of Sonos households own more than one product — a proportion that has held steady for five years now (as far back as disclosures are available).

Repeat purchases mean two things: households are loyal to the brand, and their lifetime value grows over time. But don’t take it from me. Take it from the owner of an installation business with 45 years of experience in the audiovisual industry:

We have found that when someone works with Sonos, understands Sonos, they understand what music they can bring into it, they never go back. It's hard to move them away from it to think about anything else, and we end up even retrofitting a lot of their other homes.

Nobody forces these people to buy more speakers. They like the product, so they add to the system. When they add to the system, the sound experience improves. We see this in higher NPS scores for multi-product households. When the experience improves, they’re more likely to do it again. That’s how we arrive at a steadily increasing number of products per home.

2. Word of mouth drives customer acquisition

A great brand doesn’t need to advertise as much because existing customers are the sales force. Sonos has work to do, but it’s headed in the right direction: word of mouth is the #1 source of new household acquisition.

The great Nick Sleep once wrote, “There are very few business models where growth begets growth.” Sonos looks to be one of those few, thanks to the millions of households who advocate for the brand to friends and family.

The trend up and to the right was interrupted in 2022 due to shortages in the Installer Solutions channel, a key source of new households.

Referral-driven growth is more durable than other types of growth. And if we zoom out, another interesting theory takes shape. Far from disrupting Sonos’ business with the launch of Alexa in 2014, Amazon accelerated adoption of smart speakers across the board. Sonos took nine years after shipping its first product to reach 2.2 million households. In the next eight years, it entered 11.8 million. The brand was before its time.

A 17-year streak of revenue growth in consumer audio should not be discounted (though the 18th appears unlikely). It’s the product of a culture of innovation and a commitment to quality. It also proves new households spend more over time. ~40% of new product registrations each year are attributable to existing households.

With more households acting as brand ambassadors, new households are acquired at a lower cost to the company. While LTV / HAC1 remains sub-optimal in aggregate, a positive trend is clear, and I expect the current dynamic (rising LTV, declining HAC) to persist over the long term.

Why do I expect it to persist? For one, 5.6 million households still have one product. If these households reach the average of 4.30 products typical of a multi-product household, it represents an incremental ~$5 billion revenue opportunity. And Sonos doesn’t have to acquire these households again.

3. Households are willing to wait, and pay up

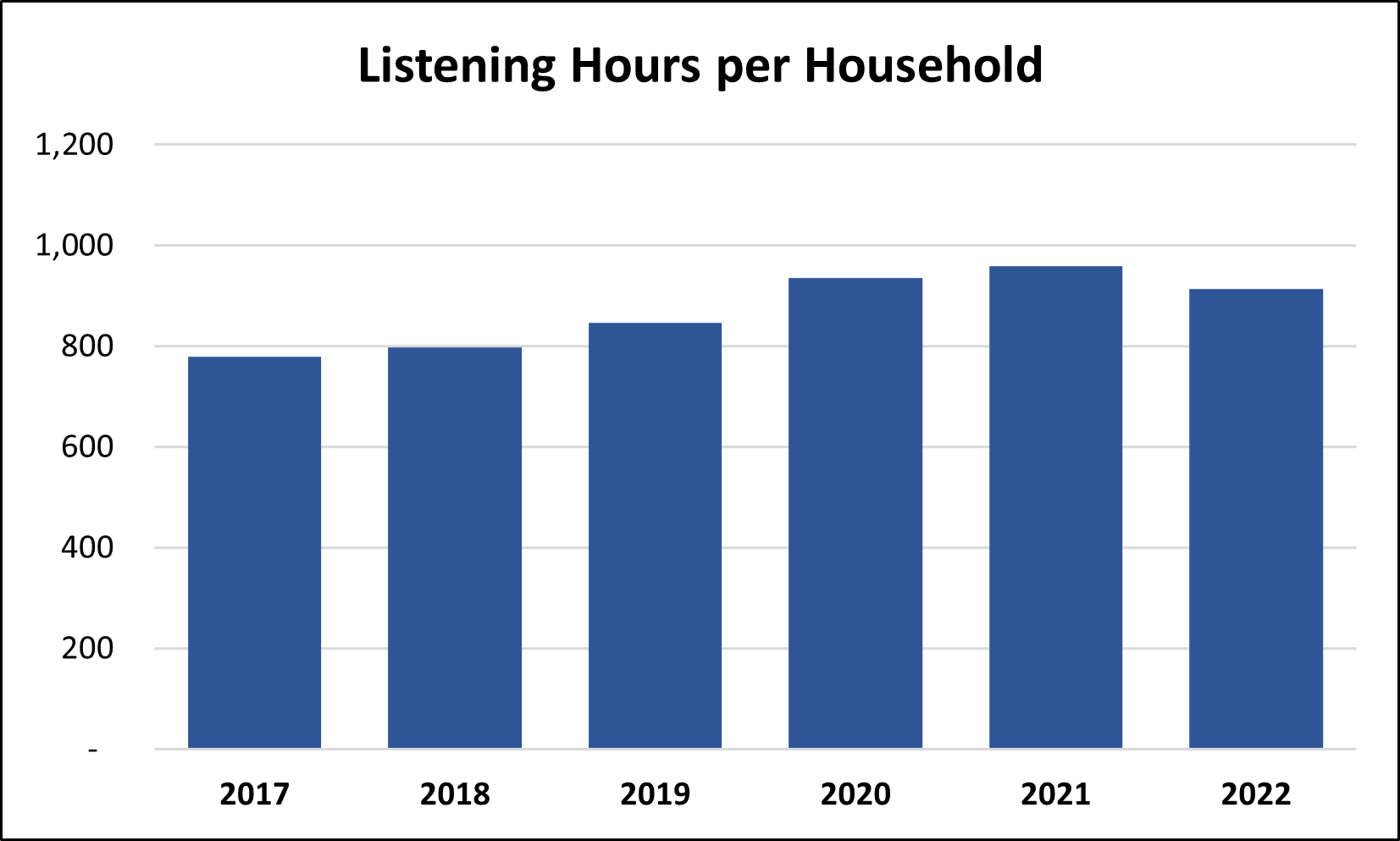

A Sonos speaker isn’t like a Meta VR device. People don’t use it once or twice before letting it collect dust. Households use Sonos speakers for ~2.5 hours a day on average, and over 90% of all Sonos speakers ever sold (dating back to 2005) remain in use today.

The longevity of Sonos products is a major differentiator of the brand. As Patrick Spence noted in the company’s first earnings call back in 2018:

We are the only company I'm aware of where people add more to their system over time versus replacing previous purchases.

Product longevity is essential to Sonos’ strategy. The game is to capture the premium end of the market. People aren’t willing to pay top dollar if the product doesn’t last a long time. Luckily, Sonos products do — which makes people willing to pay a premium price, and wait for it if necessary.

Gross margins north of 40% (above Apple) in a commoditized product category tell you all you need to know: people pay for the brand.

Further, consumers are willing to wait for out-of-stock products. During a prolonged period of product constraints in 2021 and 2022, consumers continued to wait for Sonos to return to stock.

From Q2 2021 call:

One of the things we've looked at over the past few months, not even relative just specifically to Roam, but overall on products is what the cancellation rate of orders looks like because we've been in a situation where products like Arc or Amp have had delays along the way. And we are seeing incredible strength in terms of those orders. They do not appear to be perishable. In any way, people do not come back and cancel.

From Q4 2021:

We've been dealing with some supply chain issues throughout the year. So we've seen on particular products how the behavior has been, and we continue to see very low cancellation rates on those orders… We haven't seen anything in the market that makes us believe people are moving to some other product that's out there.

From Q2 2022:

Our back orders are generally cancelable. We have tracked those through the last multiple quarters, and we have incredibly low cancellation rates and nothing about those cancellation rates has changed to this point.

It all points to Sonos being a considered purchase. It’s not, “Let’s buy a speaker.” It’s, “Let’s buy a Sonos.” That’s good positioning.

4. Sustained share gains in core markets

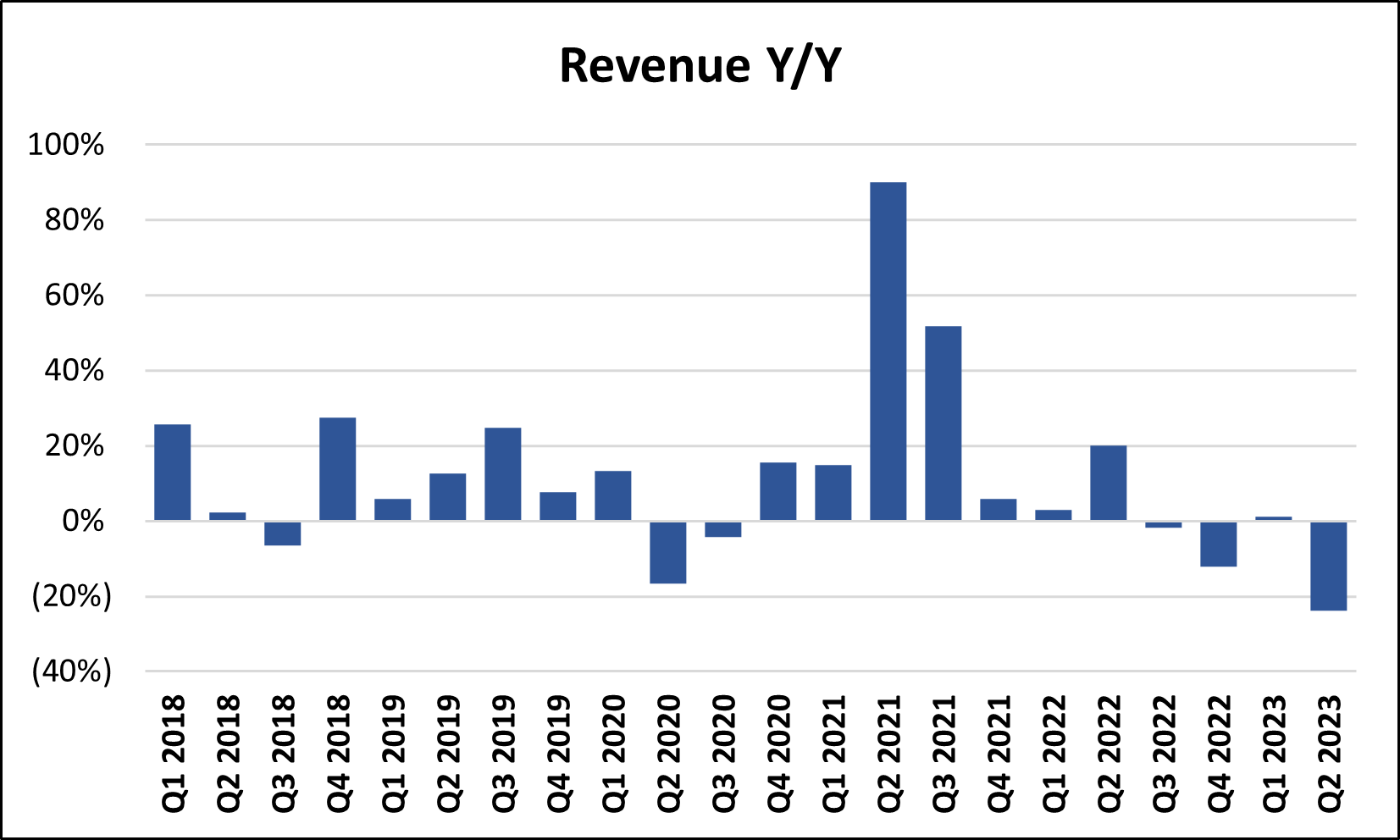

A common misunderstanding is that Sonos should report smooth revenue growth. Unfortunately, that’s not how consumer purchase patterns work. If consumers are uneasy, they’ll just hold off on buying a speaker; they’ll wait until next year or next month when they’re less uncertain about the decision.

That’s why, at times, we’ve seen Sonos report 80%+ growth and at other times, 20%+ declines year-over-year. The key is to compare it to the industry performance, not anything else.

Right now, people aren’t buying a lot of speakers. Maybe it’s because of economic uncertainty. Maybe Covid pulled forward demand. Nobody quite knows. But a multi-year view reveals things aren’t as bad as they seem; Sonos is still regularly hitting its long-term target of a 10% CAGR.

Most importantly, it continues to outpace the industry and gain dollar share in core categories — despite heavy discounting across the marketplace.

From the Q2 earnings call:

The market data that we track showed a pronounced decline in U.S. home theater sales in March, while the European home theater market remains very challenged. Our home theater share gains in Q2 show that customers are still choosing Sonos over the competition despite the deep discounts that legacy audio competitors are offering. But ultimately, we are not immune to the widespread category weakness.

This is not a new phenomenon. From the Q1 call:

We built upon our already strong share of home theater market and saw significant gains in the U.S., U.K., Germany and the Nordics, resulting in our highest share in terms of both dollars and units in 3 years. We performed well amidst the competition in the wireless speaker category as well.

Nor is it limited to this fiscal year. From the Q4 2022 call:

Our products are resonating with consumers. In Q4, we saw both sequential and year-over-year improvements in our home theater market share in the U.S., U.K., Germany and the Nordics, reaching our highest level of unit and dollar share in almost 2 years.

From the Q3 2022 call:

Despite the macro dynamics of Q3, we gained or held share in key categories across our geographies, and we saw steady repurchase trends among our growing base of existing households.

And last one for you. From the Q2 2022 call:

We believe we are taking share. From everything we can see across all of our major countries, we believe we're taking share in the markets.

Market share gains amid prevailing economic uncertainty are always a positive sign.

Conclusion

There is little not to like about a brand with customers that buy more over time, endorse it to friends and family, and are willing to pay up (and wait for products to come in stock). Add evidence of sustained market share gains amid a difficult external environment, and the story becomes even more intriguing. If I were a betting man, I’d say Sonos is a brand that can compound.

Disclosure: I own shares of Sonos. Despite this being my third article on the company, it is a relatively small position. I just find the company fascinating. Links to my other articles below:

Lifetime Value = Gross profit per product multiplied by average products per household / multi-product household.

Household Acquisition Cost = Sales and marketing expense divided by new households.