If you would prefer to read in PDF format, click below.

Recaps are an extension of my investment process, which I liken to a continuous investigation: you accumulate evidence, assess the facts, consider probabilities, and make judgments. A single Recap will never tell the full story, but it should provide a snapshot of thinking at a moment in time.

This first edition lays out an updated thesis for my top three holdings (~60% of my portfolio). Most editions will not be “stock pitches” in this sense – they will read more as a collection of notes, commentary, and analysis – but I thought this exercise would be a useful frame of reference for future discussions. The section on Pagaya is a bit lengthy, but I hope you find it worth the time.

Feedback is always welcome. Disagreements are encouraged. And as always, thanks for reading. If you find my work useful, please consider sharing with a friend.

1. Why I Own Planet Labs | PL 0.00%↑

Planet is my largest investment, and I’ve discussed my view of the opportunity at length (see here for some of my analysis). While my original thesis could be more organized and concise, many of the points are still valid.

Planet is an early stage category creator. It collects and sells proprietary data from the largest satellite imagery network in the world. The unique value of its data is in its combination of global scale and daily refresh rate. This daily scan is a differentiated offering in the market and will drive the business over the long term.

In the near term, Planet’s tasking business (a complement to the scan) may contribute more substantially to growth. Defense agencies still dominate industry spend, and they have established budgets for specific capabilities in the domain. But, over the long term, I think the compounding value of a live Earth database is what really separates Planet from other market participants.

Planet’s data enables a variety of use cases which provide a tangible benefit to government and commercial customers. The product is sticky, but extended sales cycles have led to challenges scaling the business. For one, data exists a layer below software; it requires specialized resources to assess its impact, implement, and then turn into a useful operational asset. Second, geospatial expertise is rare, and the sheer volume of Planet’s data can be overwhelming. Third, as I mentioned, governments still dominate industry spend, and governments move / procure slowly.

To combat these headwinds and accelerate growth, Planet is (1) developing downstream data products to reduce the need for geospatial expertise, (2) building a platform for developers / users to more easily fuse different datasets and stream data / analytics directly into their preferred workflows, and (3) scaling the sales force. These investments manifest mostly on the income statement.

Planet is also investing (via the cash flow statement) in new data acquisition infrastructure (new satellites / sensor types) to open new markets and unlock upsell opportunities. More data and the fusion of multiple sensors commonly yields a 1 + 1 = 3 effect, which delivers a better product to customers.

Both areas of investment, over time, should support durable growth and increasing operating leverage. Planet, as with most data businesses, benefits from naturally advantaged economics as its cost to acquire data is largely fixed. The rapid expansion of gross margins is evidence of this dynamic.

Further, product and platform investments should improve LTV and reduce CAC over time. Moving up the stack (selling software on top of the data) delivers more value to customers and creates expansion opportunities at a lower cost; self-serve platform capabilities reduce the time salespeople have to spend nurturing and converting (especially lower-value) leads.

Additionally, Planet’s capex spend benefits from an underlying trend of exponential improvements in the cost-performance of satellites. SuperDoves are ~1,000x more capable than their predecessors, producing more data and higher quality data at around the same cost. Pelicans report significantly better performance across every metric (resolution, capacity, revisit rate, and latency) at roughly half the cost of their predecessors (SkySats).

People often question the wisdom of Planet’s investments when they see the size of its losses. I think this view is shortsighted. While the current level of investment no doubt obscures the company’s potential profitability, it also has a viable path to significant ROI and deepens its competitive positioning.

I would go so far as to argue an internet-native business model with a unique value proposition and potential for increasing returns to scale would be foolish to not invest heavily in accelerating the realization of the market opportunity.

Importantly, the balance sheet affords the flexibility to maintain these investments without regard for external opinion. Since going public over three years ago, Planet has only used around half of its proceeds and still has ~$240M in net cash. Management has committed to reaching free cash flow breakeven while keeping a “9-figure” cash balance, and the current trend points to this outcome as achievable.

Competitive analysis is the heart of good investment analysis, and an area where investors commonly misunderstand Planet. Competition, in my view, is not a near-term concern. High-resolution tasking is a competitive market, but the daily scan, which accounts for ⅔ to ¾ of total revenue, is a virtual monopoly. Selling the scan is a question of technical capability (which is constantly improving) and what value it can deliver (which is continuously growing), not competitive dynamics.

The scan has operated without peers for over seven years now, and while some other players are making noises in the same direction, the real alternative today is free data from public missions. More often than not, however, these public missions are not competitive but complementary; they support Planet’s product development. New commercial entrants present a similar complementary opportunity; look no further than SynMax for an example of how partners leveraging multiple data sources can create a better product for customers and grow the total market opportunity.

It’s also worth noting the value of Planet’s archive; would-be competitors can’t go back in time to replicate this asset. And while most analysts assign little value here, I think it’s an incredibly valuable machine learning asset and will support product / platform development efforts for years to come.

The long term opportunity for satellite data rests on application layer companies fusing multiple datasets (both satellite and non-satellite) to deliver a scalable solution to (generally vertical-specific) end customers. Planet’s future enterprise value depends on its ability to arm these partners with the tools and infrastructure to do so, and its strategy is centered on capitalizing on this opportunity.

Under such a scenario, I expect aggregate demand for satellite data, and Planet’s platform growth, to vastly exceed market expectations. Today, however, this is far from reality. Spending remains concentrated in defense and intelligence, and the timeline for change is highly uncertain. The commercial market has even receded in the last few years.

But zooming out, this is a story of inevitable change driven by rapid improvements in satellite performance, the explosion of satellite data, and the advent of AI. An investment in Planet is based on growth in the size of the pie, not Planet taking a larger slice – and I think this endgame is inevitable given a long enough time horizon.

2. Why I Own Xometry | XMTR 0.00%↑

Xometry is a digital-native marketplace for custom manufacturing. It has pioneered a novel user experience that leverages AI on top of a vast dataset of historical transactions to offer a range of instant prices and lead times from simply uploading a CAD file to the website.

As I define it, “digital-native” means the end-to-end transaction occurs entirely online, eliminating any back-and-forth between buyer and supplier. Legacy marketplaces that facilitate RFQ processes don’t qualify: the second a buyer hits the “Request a Quote” button, they are back in the analog world.

My investment in Xometry is based on three key assumptions:

Digital-native marketplaces will expand their share of industry transaction volumes.

Xometry is the clear leader among these types of marketplaces.

The business benefits from network effects which serve to extend its advantage.

My conviction in the marketplace opportunity in custom manufacturing is partly based on my analysis of Bill Gurley’s framework of how to evaluate digital marketplaces. To recap (just a few of the ten dynamics assessed):

The industry is highly fragmented on both the supply and demand side.

Instant pricing and an end-to-end digital purchase process offer a radically superior user experience compared to the manual back and forth typical for custom parts procurement.

The economics are advantageous. Buyers benefit from a simplified procurement workflow and access to thousands of suppliers; suppliers can monetize excess capacity and improve machine uptime by accessing new sources of demand.

In my original pitch, I cited Xometry’s unique data as the source of its advantage. In hindsight, I was wrong. Data is important but not a differentiator – it’s the cost of entry. Data is a prerequisite to providing a digital-native experience, but Proto Labs Network, Fictiv, and other marketplaces have shown they can facilitate a similar user experience.

What differentiates Xometry is the size and rapid expansion of its network. Let’s consider a few examples. Fictiv is private, so it’s difficult to triangulate precise scale, but the website claims 150,000+ hours of monthly machining capacity; if we assume each supplier has two machines with 160 hours of monthly capacity (40 hours per week), that implies a network of around 500 suppliers. Proto Labs Network claims 250+ vetted manufacturing partners on its website. Both are significantly less than Xometry’s 4,000+ suppliers.

On the demand side, Fictiv’s website notes 18,000+ customers. Proto Labs Network served ~44,000 unique customer contacts (individuals who could be from the same company) through the first three quarters of 2024, a decline from ~53,000 in 2023 and ~56,000 in 2022. Xometry, meanwhile, reports ~65,000 active buyers, growing 25% YoY.

Networks are ultimately differentiated by scale, and Xometry clearly outpaces the competition here. The core marketplace is healthier than ever – the number of buyers is growing, buyers are spending more over time, and new materials, finishes, and processes are routinely added to the menu. If you’re unfamiliar with the terminology, the basic concept is no different than Amazon expanding from books to CDs, video games, and so on.

As Xometry expands horizontally, it can attract suppliers from the extensive supplier database assumed via the Thomas acquisition. And as selection widens, Xometry offers a more compelling value proposition to buyers who can source a greater variety of parts from the same online destination – “one throat to choke”, as Randy Altschuler refers to it. Over time, this should allow the company to continue to attract new customers and capture greater wallet share among existing customers.

Xometry is the largest digital marketplace in an industry primed for marketplace disruption and early in its inevitable digital transition. The scale of its network creates an advantage which should serve to extend its market leadership over time. The founders remain substantial owners of the equity and have shown an ability to execute. The business continues to accumulate share gains amid a tough manufacturing environment, and I see no reason why this trend would slow down moving forward.

3. Why I Own Pagaya | PGY 0.00%↑

“What we are building here is one of the most unique infrastructure platforms for credit generation in the United States.” – Gal Krubiner, Co-founder & CEO

Pagaya is a bet on AI’s transformation of lending. My rough thought process is as follows:

U.S. consumer credit markets are broadly inefficient and inaccessible.

AI can more precisely measure default risk and expand access to credit.

Banks are ill-suited to build and deploy the necessary technology in-house.

Pagaya’s network can effectively fill that technology void and expand its share of loan origination volumes over time.

The business model and unit economics can scale profitably.

Pagaya is a “riskier” investment in that the range of outcomes is wide; it’s a difficult problem the company intends to address, and many have failed in their attempts. But, investment decisions are based on a risk-reward tradeoff, and I think the potential reward here more than compensates investors for even the (improbable) risk of total loss.

US consumer credit markets are broadly inefficient and inaccessible

Core to the thesis is a somewhat abstract concept: the idea that a significant, creditworthy population exists outside the bounds of traditional lending markets. I could try to illustrate this inefficiency with statistics, but I would rather appeal to logic.

Borrowers face high search costs and a lack of information as they navigate a highly fragmented landscape of lenders. Lenders, meanwhile, struggle to accurately underwrite risk using a credit score as the primary input. Strict market segmentation (e.g., subprime vs. prime) exacerbates this problem by limiting true price discovery; the tens of millions of Americans who are credit invisible, have thin files, or even subprime scores are often simply out of luck.

In many ways, a FICO score acts as a filter today; lenders will only target segments with a 680+ score, for example. But logically, this makes no sense. Why would we limit the inputs to a critical economic decision at a time when vast alternative datasets are available, and sophisticated modeling (that only works when applied to vast datasets) invariably produces a better decision in almost every other domain of business?

It’s no secret traditional rules-based regression models fail to effectively price risk for a sizable segment of the population. Countless companies were founded on this basic premise – but what has proven extremely challenging is executing on the opportunity and scaling a viable business model.

AI can more precisely measure default risk and expand access to credit

It’s difficult to reconcile the extreme bullishness around AI with the broad skepticism of its application to lending. The essence of lending is a prediction of who will pay you back, and who won’t pay you back. AI is a highly effective, infinitely scalable prediction machine.

Jeff Bezos recently shared how he views AI (link to full interview):

Modern AI is a horizontal enabling layer… These kinds of horizontal layers, like electricity and compute and now artificial intelligence – they go everywhere. I guarantee you there is not a single application you could think of that isn’t going to be made better.

Why would lending be the exception? I understand there is no shortage of charlatans in the category – plenty of companies have made empty claims about a better credit box – but it’s difficult to argue with the overwhelming logic behind AI consuming rules-based models over time. It’s inevitable, and we are at the very beginning of witnessing its impact.

It’s impossible to stand here and provide firm evidence that Pagaya is the answer, that it has cracked the code and separates risk better than any other model or lender. It would be foolish to even attempt to make such an argument today. But, I will argue the network infrastructure Pagaya is building is well-suited to execute on the opportunity, and its expansion in recent years speaks to an ability to extend performant credit to an underserved segment of the population.

Pagaya has now originated over $26B in second-look loans. In 2024, it will report north of $10B while capturing ~70% of the personal loan ABS market. That is $26B of loans ($10B just in the last year) enabled by a unique AI model, on top of a unique supply of data, offered to consumers turned away by traditional underwriting models. I think people underestimate the significance of this statement.

The performance of this loan book, in aggregate, has been adequate: some have beat expectations, some have met expectations, and others have fallen short of expectations; but, the credit quality has been good enough; if it weren’t, previous investors would not be lining up to allocate more capital, and Pagaya would not be in the position it is today as the benchmark issuer.

Contrary to popular belief, a more precise model will never eliminate risk, but it should dampen the volatility of outcomes over time. Investors (in the equity) must simply be confident in two things: (1) that Pagaya’s loan performance will increasingly converge on the predicted outcome as the network collects more data and enhances its models and (2) that occasional underperforming vintages will not impair the company’s ability to raise capital. Unfortunately, these are difficult to measure from the outside.

Banks are ill-suited to build and deploy the necessary technology in-house

If Pagaya’s technology allows it to more accurately underwrite a broader base of consumers, wouldn’t banks simply replicate it? The short answer is some of them will, but most of them can’t. Banks and traditional lenders looking to develop and deploy an AI lending model need to first overcome some structural headwinds.

Most banks operate on outdated, siloed tech stacks incapable of integrating and processing the data required for modern AI; those same banks also lack the commitment, budget, and technical staff needed to reconfigure and optimize the system.

Outside of the JP Morgans of the world, most banks also lack a massive volume of training data; the data corpus is limited by the size of the loan book. A network like Pagaya, with visibility into programs across many lenders, can more effectively solve this data aggregation challenge.

I could go on about talent gaps, cultural challenges, etc., but really, it’s simple: API-led, plug-and-play (and compliant!) solutions are a natural fit for how most banks will eventually deploy AI in lending. Networks like Pagaya can aggregate data across a broad base of lenders, spread R&D costs across its partners, and prioritize iteration and constant improvement.

Pagaya’s network can effectively fill that technology void and expand its share of loan origination volumes over time

Before we dive into how the network grows, it’s important to understand the constraint: the mutual dependency of a two-sided network. Pagaya is in the business of connecting borrowers and lenders (and by lenders, I mean capital providers, not its lending partners). If it can’t source borrowers, no amount of capital can grow the business. Likewise if it can’t secure capital, borrowers are a moot point – the business can’t grow.

For the network to expand, it has to first demonstrate a compelling value proposition to both demand-side and supply-side partners. So, let’s start there.

Lending Partners: For banks, captive auto lenders, and fintechs, Pagaya’s second-look decisioning allows them to attract and retain customers they would otherwise turn away, while offloading the credit risk. Pagaya also increasingly enables partners to offer a broader suite of credit instruments to their customers; according to the company, the most commonly cited benefit among partners is increasing customer lifetime value.

Investors: Investors come for the ability to deploy capital at scale across diversified credit assets, and stay for continued delivery of an acceptable return.

The strength of the value proposition is most evident from the network’s rapid expansion. As is typical of network effects, this expansion feeds back into growth. More lending partners means more opportunities for asset creation, a boon for investors. More investors translates into an ability to convert more borrowers, a positive for lending partners.

Growth is essential to the investment thesis; a network either grows or dies. The most important input to growth is network volume (i.e., the volume of loans originated via Pagaya). Growing network volume is a function of increasing application flow, improving conversion rates, or both.

Network Volume = Application Flow x Conversion Rate

There are a variety of ways to grow application flow, but mainly, Pagaya can (1) add more lending partners and/or (2) grow its share of volume among existing partners.

Pagaya has excelled in the first department. Against a long stated goal of onboarding 2-4 new partners a year, Pagaya brought in six new partners in 2022; four in 2023; and two YTD Q3 2024. Some people might jump on what looks like a declining trend, but the reality is Pagaya is moving up-market.

The last three lenders to onboard are US Bank (a top 5 bank), Elavon (its payments subsidiary), and OneMain Financial (one of the largest subprime lenders in the US). Another top 5 bank is in the midst of onboarding, and while these partners may take longer to onboard (~18 months in the case of US Bank), they present attractive opportunities to expand horizontally over time.

With a window into >$1T of annual application flow already, signing new partners is not the immediate constraint on growth; near-term growth depends more on ramping up existing partners, an area where the company has also been successful over time.

It’s not until the second or third year post-onboarding that Pagaya starts to really expand its share of volumes and monetize the partnership. Klarna, for example, is only now rapidly scaling volumes after onboarding in 2022. Recent additions such as US Bank / Elavon and OneMain Financial should provide platforms for growth years into the future. The clear trend is a growing share of originations among partners – it just takes time.

New offerings such as the pre-screen product are effective means of expanding the network’s surface area and gaining share of total originations. Whereas Pagaya’s flagship products are focused on new customer acquisition, pre-screening programmatically targets existing customers.

Pagaya’s strategy, over time, is to take on more and more of a bank’s end-to-end lending value chain. We’re not there yet, but as it lands more logos, deepens existing partner relationships, and enhances its credibility in the overall banking sphere, I think the company has a right to expand its share of partner originations even more.

Once again, this expansion naturally feeds back into growth. As the network widens its aperture and assembles a more comprehensive dataset of consumer creditworthiness (across asset classes and up and down the credit spectrum), it should allow Pagaya to optimize conversion rates, the second key driver of network volumes.

For several years now, Pagaya has kept conversion rates sub-1% in order to manage risk. In practice, this means loans are priced higher (with a “margin of safety” of sorts) than the “baseline” model might call for, and as a result, fewer customers accept those offers. This risk management effort has paid off: cumulative net losses (CNLs) for 2023 personal loan and auto vintages are down 20-40% and 30-50%, respectively, versus peak 2021 levels.

Conversion rates, in the long run, are downstream of model accuracy. I think it’s reasonable to expect the core AI to improve as the data corpus grows and specific model instances are tailored to unique application flows. Management once highlighted potential for 20-30% improvements to conversion rates annually, and while that seems ambitious (and does not factor into my investment case), it is worth noting. Such a move would drive immediate, substantial growth, even holding application flow constant.

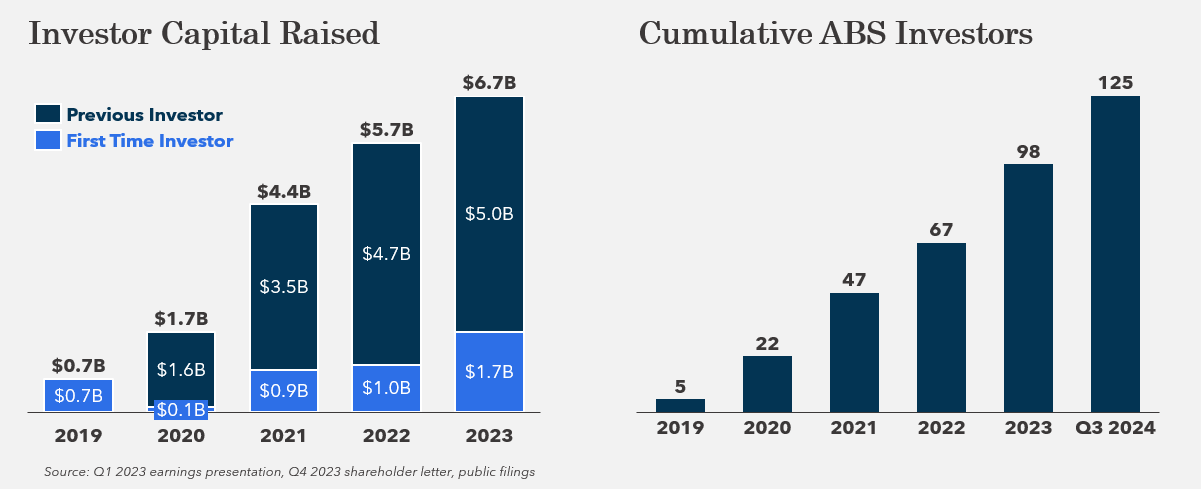

Stepping back, I think the network will grow, not die. Application flow will almost certainly continue to grow, and I am optimistic conversion rates will improve but am not relying on it to make the investment case. The constraint, or the major uncertainty as I see it, is supply, or fundraising. How much growth can capital markets accommodate?

Here, you have to have a bit of blind faith, but the most bullish evidence is (1) increasing allocations from previous investors and (2) steady growth in the total number of investors.

We will ultimately have to wait and see here – it’s difficult to predict capital markets activity – but capital is a commodity, and one that seems increasingly abundant. Pagaya benefits from the secular growth of private credit as an asset class, and I think it’s fair to assume it can capitalize on that tailwind given its unique value proposition.

The business model and unit economics can scale profitably

The many questions surrounding the business model are valid; the unit economics don’t work as they stand. Risk retention requirements outweigh the fees earned on network volume, so Pagaya is repeatedly forced to raise debt and/or dilute equity to fund its expansion.

Growth has proven counterproductive to the financial model, and when you add to that a worrying trend of rising credit impairments, it’s not difficult to see why the stock has suffered. But, the immediate financials never paint a complete picture, and I think these challenges will prove to be transitory.

Pagaya is at an inflection point in its ability to (1) improve take rates and reduce risk retention such that incremental network volume contributes positive cash flow and (2) manage its credit portfolio such that future impairments don’t damage the income statement to the same extent.

The recent move to diversify funding has led us to this inflection point. Historically, Pagaya has relied on ABS markets for the vast majority of its funding, and regulation requires ABS issuers to retain 5% of the asset pool (with some nuance). With net take rates at sub-4% for most of 2021 to 2023, the company had to put up more and more of its own capital, which was often obtained via unattractive but imperative financing.

From Q3 2021 to Q3 2024, Pagaya cumulatively generated $45M of operating cash flow. Investing cash flow? Negative $1B. However, the economics have changed. Take rates have climbed to 4.3%, with room to go higher. And growth in privately managed funds (as a result of the Theorem acquisition), new forward flow agreements, and more pass-through securitizations has already reduced risk retention to the target range of 2-3%.

All of a sudden, what was previously a business with sub-4% take rates and 5% capital investment is now a business with plus-4% take rates and 2-3% capital investment. Cash flow won’t knock anyone’s socks off in year one, but that’s the start of a real business. Management is resolute that they will deliver GAAP profits in 2025. As it begins to show operating leverage below the line, the financial profile should improve considerably.

By that point, the market will understand the potential and price it accordingly. The window of opportunity exists today because the market lacks faith in the strategy and assigns a low probability of the company becoming a more stable, cash-generative business. Again, I think this is shortsighted and based on a view of the past, not the future.

Personal loans, Pagaya’s most mature segment, already demonstrates a 6.6% take rate with only 2-3% risk retention. The standalone economics work, volumes are still growing, there is even room to build on that take rate, and over time other asset classes will converge to similar economics.

As for credit impairments, some level of impairment is inevitable for a business involved in lending. But, the significant and rising impairments we’ve seen of late are a symptom of one-off decisions and investments made in a time of heightened uncertainty, when management bet the expansion of the network would prove to be more important to the long-term value of the enterprise than being overly judicious about the risk of any individual security.

Take it from Gal Krubiner when asked about the impairments on the last earnings call:

Let's start from the past. What is Pagaya? Pagaya’s business is a network. In a network, you need to make sure the network is flowing all day, every day, no matter what. That's our responsibility to both our partners and investors to deliver to them the best flow and the best return. In 2023, which was a unique time when there was a really big gap, we filled the gap. That is an investment.

We did that because we believe that the investment we made is going to end in a massive outcome, which is the enterprise value you see here today – 31 different partners, US Bank, many others, and at the same time, happy investors from 2023. Every investor you're going to speak with that invested in a Pagaya security in 2023 will tell you, ‘great platform, great returns.’ And these are the investors that are looking now to open their deployment, as you heard David speaking about. So we are the first choice, and we did all of that to get ready for this particular moment in time to make sure we are capturing that momentum very well.

I’m comfortable with this attitude toward the business, especially as ABS markets in 2023 were still digesting the impact of a rapid increase in interest rates and a sharp rise in delinquencies. Pagaya accepted lower spreads and greater risk to grow the network, and it worked. Network volumes grew 14%, and the company added 31 investors. The reality of that risk is now being confronted, but it’s a function of circumstances that are now history.

As the pool of risk retention assets declines as a percent of volume and take rates increase as a percent of volume, even impairments of similar relative magnitude to those suffered from 2023 vintages will have considerably less impact on the consolidated financials.

In the near-term, the stock will undoubtedly suffer if they report another sizable impairment in Q4 (a likely outcome given they will book remaining 2023 impairments then). But again, the time to buy is not when everything looks rosy. The time to buy is when the immediate financials paint a lousy picture, but 18 months from now should look a lot different. I very much believe that’s what the case is here.

Conclusion

Pagaya is building a database of US consumer creditworthiness. That database integrates into the loan origination systems of 31 lenders today (representing ~$1T annual application flow) and will reach more lenders over time. That database also extends across asset classes and scales without limitation. And it enhances the customer experience by providing an instant credit decision in a digital-native format.

The founders are young, mission-driven, and retain meaningful equity stakes. They have brought on experienced executive talent (Sanjiv Das, for one) and have shown a willingness to make difficult decisions in the interest of the long term at the expense of the short term.

Early private investors (Oak HC/FT and Viola Ventures) remain sizable owners after more than two years as a public company, and I bet they know the business better than anyone. The signs point to opportunity – it’s just a matter of looking out beyond the immediate financial picture.

Thanks for the article! Any opinion on the short report?

Impressive stuff. Thank you for sharing.